Chapter 1 : Islamic Banking and Financial System

MEANING OF ISLAMIC BANKING

- Banking business whose aims and operations do not involve any element which is not approved by the religions of islam (IBA 1983).

- Islamic financial instituitions that based on syariah principles which avoidance of riba, gharar and maisir.

ISLAMIC BANKING IN THE EARLY DAYS OF ISLAM

•The only known organised islamic financial instituitions during the time of prophet (saw) was call "baitul mal"

•Objective - mange the financial affairs of the islamic state-not generally accept deposits nor grant loans.

•Public money and valuables werw kept by trustworthy individuals such as the prophet (saw) and zubair bin al-Awwam

•The prophet (saw) was entrusted by the people of mecca with safekeeping their money

•This concept , te trustee did not have the right to use the funds

•Zubair bin al -Awwam chose to only receive money as a loan (qard) - had a right to make use of it and had the obligation to return it intract

•Ibnu Abbas was noted to have transfered some money to Kufah. so was Abdullah Bin Zubair in Mecca, who sent money to his brother Hisab Bin Zubair, who lived in Iraq - activities related to remmittance and bills of exchange.

•The use of cheque was widely known with the growing trade between the cities of syam and yaman - with this cheque the beneficiaries would be able to collect from Baitulmal a quantity of wheat imported from Egypt

•There were already a few individuals who practiced banking functions although not performing comprehensively

BANKING FUNCTIONS DURING THE PROPHET ERA

- To channel financing

- To transfer money

- To accept deposits

BANKING PRACTICE DURING BANI UMAYYAH AND BANI ABBASIYAH

•In the prophet (saw) time, banking functions were undertaken by individuals – one man one function basis.

•In the era of Bani Abbasiyah , these three banking functions (were undertaken individually) –one man multi function banking practice

•When various types of currencies were in circulation , special expertise was required to distinguish one coin from the others.

•Each coin its own precious metal content, hence its own value.

•Special expertise – naqid, sarraf , and jihbiz – the impetus of the practice of money exchange

•The role of bankers began to pick popularity during the reign of Muqtadir – most wazirs had their own bankers.

•A milestone in the development of banking practices at the times- wide circulation of saq (cheques) as an instrument of payment.

•Money could be transferred across countries without a need to move the physical money

ISLAMIC BANKING IN THE MODERN ERA

Year

Name of Bank

1960-1970

Mit Ghamr, Local Saving Bank, Egypt (1963 )

Lembaga Tabung Haji Malaysia

1970-1980

Nasser Social Bank, Egypt (1971)

Islamic Development Bank, Jeddah (1975)

Dubai Islamic Bank Dubai (1975)

Faisal Islamic Bank Sudan (1977)

Bahrain Islmaic Bank , Bahrain (1979)

1980-1990

Bank Islam Malaysia Berhad, Malaysia (1971)

Islamic Bank , Bangladesh (1983)

Al-Baraka Group in Countries (1982)

Qatar Islamic Bank (1983)

Daral Mal Islamic Trust, Geneva (1984)

AHZ Global Islamic Finance, UK (1989)

1990-2000

Islamic Bank of Brunei (1993)

Bank Muamalat Malaysia (1999)

•There are over 300 islamic Financial institution worlwide across 75 contries

•According to the Asian Banker Research Group, The World's 100 Largest Islamic Banks have a set an annual asset growth rate of 26.75% and the global islamic finance industry is experiencing average growth of 15-20% anually

DEVELOPMENT OF ISLAMIC BANKING IN SOME MUSLIM COUNTRIES

- Bahrain

- Sudan

- Pakistan

- Turkey

- Iraq

- Egypt

Chapter 2 : Financial system in Malaysia

Definition

- The Malaysian financial system is made up of two components, the financial intermediaries and the financial market.

- BNM and the banking industry consisting of commercial banks, Islamic banks and investment banks make up the banking system. In Malaysia, Islamic and conventional banking systems coexist and operate in parallel.

Financial System

- Financial Intermediaries

- Unit trusts

- Cooperative societies

- Leasing and factoring companies

- Housing credit institutions

2. Financial Market

- Money market

- Foreign exchange market

- Equity market

- Derivatives market

- Bond market

Banking System

- The banking system has been the largest financial intermediary in terms of total assets. All financial institutions under the Banking and Financial Institutions Act 1989 (BAFIA) The system comprises the following:

- BNM(Bank Negara Malaysia)

- commercial banks

- investment banks

- Islamic banks

1. Bank Negara Malaysia

- Objective

- Promote monetary stability and a sound financial structure.

- Act as banker and financial adviser to the government.

- Issue currency and keep reserves to safeguard the value of the country’s currency.

- Promote the reliable, efficient and smooth operation of national payment and settlement systems and to ensure that the national payment and settlement systems policy is directed to the advantage of Malaysia.

- Influence the credit situation to the country’s advantage

- Function

- Implementation of monetary policy.

- Controls the nation's entire money supply.

- The Government's banker and the bankers' bank ("Lender of Last Resort").

- Manages the country's foreign exchange and gold reserves and the Government's stock register;

- Regulation and supervision of the banking industry

- Setting the official interest rates- used to manage both inflation and the country's exchange rate - and ensuring that this rate takes effect via a variety of policy mechanisms

2. Commercial bank

- Initially, commercial banks in Malaysia were governed by the Banking Act 1973. This was subsequently replaced by the BAFIA in 1989. The BAFIA combined the Banking Act 1973 and the Finance Companies Act 1969 under a single legislation. Following the merger of local banks and finance companies into 10 local banking groups (as at May 2008, there were nine local banking groups), the functions of finance companies, such as hire purchase and leasing activities.

- Functions

- Mobilise savings through current, savings and fixed deposit accounts and other financial instruments.

- Grant loans and advances

- In the form of providing various credit facilities to business enterprises and private individuals for working capital, investment and consumption.

- Provide trade financing facilities

- To assist in promoting cross-border international trade and domestic financing facilities.

- Provide treasury services

- Dealing in government securities and treasury bills and other money market instruments as well as foreign exchange transactions.

- Facilitate cross-border payment services

- Providing fund transfers and remittance services within Malaysia and overseas for business as well as personal needs.

- Provide custody services, e.g., safe deposits and share custody.

- Provide wealth management services and sales of investment and insurance products and financial planning services,

- Provide hire-purchase and leasing facilities.

- Provide any other such business that BNM, with the approval of the Ministry of Finance, may prescribe from time to time.

3. Investment bank

- Investment banks are institutions which were transformed from merchant banks, stockbroking companies and discount houses on 1 January 2007. As a point of reference, the conventional role of discount houses can be described as keepers of liquidity for the banking system. Generally, discount houses specialise in shortterm money market operations.

- Functions

- Sales and trading

- On behalf of the bank and its clients, a large investment bank's primary function is buying and selling products. In market making, traders will buy and sell financial products with the goal of making money on each trade. Sales is the term for the investment bank's sales force, whose primary job is to call on institutional and high-net-worth investors to suggest trading ideas (on a caveat emptor basis) and take orders. Sales desks then communicate their clients' orders to the appropriate trading desks, which can price and execute trades, or structure new products that fit a specific need.

- Research

- The equity research division reviews companies and writes reports about their prospects, often with "buy" or "sell" ratings. Investment banks typically have sell-side analysts which cover various industries. Their sponsored funds or proprietary trading offices will also have buy-side research.

- Risk management

- Risk management involves analyzing the market and credit risk that an investment bank or its clients take onto their balance sheet during transactions or trades. Credit risk focuses around capital markets activities, such as loan. syndication, bond issuance, restructuring, and leveraged finance.

4. Islamic bank

- Islamic banks are financial institutions that operate within the framework of Islamic principles and laws. The objective is to implement the economic and financial principles of Islam in the banking arena.

- The Islamic Banking Act 1983 defines Islamic banking business as banking business whose aims and operations do not involve any element which is not involved by the religion of Islam.

- Basically, Islamic banks are founded and based on Shariah principles that include but are not limited to the following main principles:

- Avoidance of riba (interest element),

- Prohibition of gharar (uncertainty, risk, speculation),

- Focus on halal (religiously permissible) activities, and

- A general quest for justice and other ethical and religious goals.

Non Banking Finance Intermediaries

- The key players within this segment of the financial system are pension and provident funds, insurance companies and development financial institutions. Non-bank financial intermediaries (NBFIs) can be broadly classified into five groups of institutions, namely:

- provident and pension funds,

- insurance companies (including takaful),

- development financial intermediaries, and

- other financial intermediaries, such as

- Unit trusts,

- Cooperative societies,

- Leasing and factoring companies, and

- Housing credit institutions.

a) Provident and pension fund.

- The provident and pension funds (PPFs) are a group of financial schemes designed to provide members and their dependants with a measure of social security in the form of retirement, medical, death or disability benefits. The major PPFs comprise the Employees Provident Fund (EPF) and other approved private and pension funds.

b) Insurance company.

- The insurance companies comprise general and life insurance businesses as well as professional reinsurers and insurance intermediaries, such as insurance brokers and adjustors. In addition, the takaful industry or Islamic insurance has also been established to operate alongside conventional insurance businesses.

c) Development financial intermediaries.

- The main objectives of development financial institutions (DFIs) are to promote development programmes in specific economic sectors such as agriculture, industry,international trade, small medium industries, with specific institutions set up accordingly.

- The DFIs as at May 2008 are:

- Bank Pembangunan Malaysia Berhad,

- Bank Perusahaan Kecil & Sederhana Malaysia Berhad (SME Bank),

- Export-Import Bank of Malaysia Berhad,

- Bank Kerjasama Rakyat Malaysia Berhad,

- Bank Simpanan Nasional, and

- Bank Pertanian Malaysia Berhad (Agrobank).

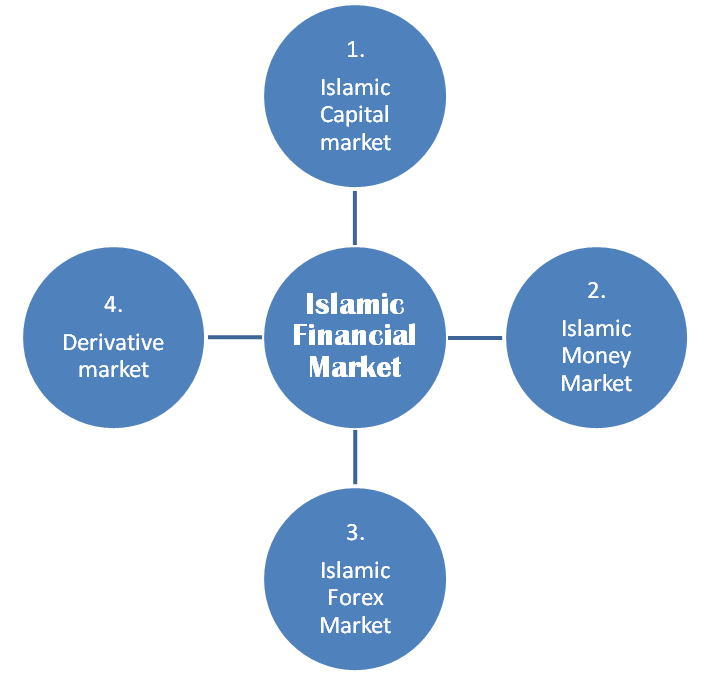

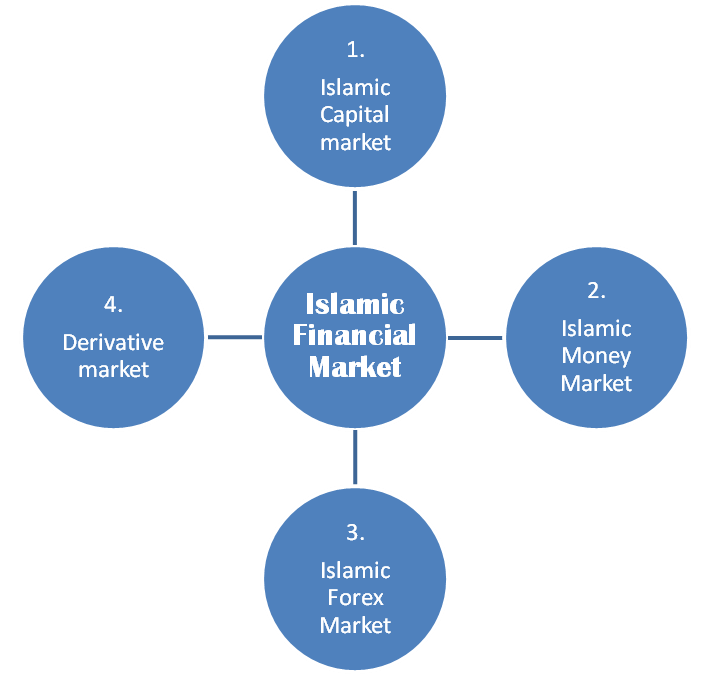

CHAPTER 3 : ISLAMIC FINANCIAL MARKET

Definition

- As in conventional finance, there are many different types of Islamic financial markets with each market having its own purpose and objectives. Similarly, there are different classifications of these markets. For example, some investors want to invest for a short-term period, while others want to invest for a long-term period. Some are risk-loving, whereas others are risk-averse. Some prefer to borrow through debt market instruments, whereas others prefer to raise funds by issuing stocks. The most common types of financial markets are as follows:

- Islamic Capital Market

- Conventional capital market, constitutes an integral part of the Islamic Financial system.

- Have two main components:-

- Debt market

- Debt securities in Islamic debt market is structured based on Islamic debt certificates like sukuk which actually resembles the features of conventional bonds representing debt or borrowed funds by the issuer.

- One of the most common sukuk classifications is based on the underlying Shari’ah contracts. These include BBA, murabahah, salam, istisna’, ijarah, musharakah, mudarabah, and wakalah. Refer figure 1.1. wa have to keep in mind that these contracts are not unique to the sukuk market.

- Debt market

Sukuk Based on Shari’ah Contracts

1) Sales-based

•BBA

•Murabahah

•Salam

•Istisna’

2) Lease-based

•Ijarah

•Ijarah Muntahiyah Bittamlik

•Ijarah Mawsufah fi Dhimmah

3) Partnership-based

•mudarabah

•musharakah

4) Agency-based

•Wakalah

- Sale-Based Sukuk

- BBA transaction

1.Sale of plantation lands (True Sale)

2.Issues sukuk BBA

3.Ijarah

- Murabahah transaction

- Purchase asset (Spot)- Asset Purchase Agreement

- Proceeds

- Sells back asset to Issuer (deferred)-Asset Sale Agreement.

- Issues Sukuk Murabahah to show obligation to pay selling price.

- Sukuk Salam Transaction

- Issue Sukuk Salam

- Proceeds & Agency

- Purchase Undertaking.

- Sukuk Istisna’ transaction

- Issuer will enter into the first Istisna’ contract with the Trustee.

- Trustee pays the purchase price(i.e cost of Istisna’ Asset).

- Trustee will thereafter enter into the second Istisna’ contract with the Issuer.

- Issuer will issues Sukuk to evidence its obligations to pay the Istisna’ Sale Price to the Trustee

bLease-Based Sukuk

- The next cluster that we will look into is the lease-based cluster,i.e., sukuk ijarah. Unlike sale contracts that transfer ownership instantaneously, ijarah contracts do not transfer ownership on its own. The most common structure of sukuk ijarah applied in the market is a sale and leaseback structure.

- Sukuk Ijarah Transaction

- Head Lease (100

- Investors

- Sub-lease (5 years).

- SPV/Issuer issues sukuk to raise funds from investors.

- SPV (directly or via company as agent) purchases the asset from supplier.

- SPV leases the asset to company (ijarah).

- Company takes delivery of the asset.

- Purchase undertaking is given to ensure redemption of sukuk.

- Company makes periodic payments.

- SPV distributes payments to investors.

- Upon maturity, purchase undertaking is exercised and asset is transferred to company.

c. Partnership- Based

- Mudarabah transaction

Investors (rab al-mal) will enter into a mudharabah arrangement with the issuer (mudharib) to invest in a business venture which is Shariah-compliant. The investors (as the sole primary subscribers) and the issuer shall participate in the mudharabah venture. Rab al-mal will provide the mudharabah capital (sukuk proceeds) pursuant to the subscription of the mudharabah sukuk (Investment Certificate) issued by the Issuer.

The Issuer will thereafter use the mudharabah capital for the purpose of the said venture which is Shariah-compliant. In a mudharabah contract, the investor and issuer will agree upfront the profit distribution that will be shared based on a profit-sharing ratio. Typically in a mudharabah sukuk, the issuer will make a Trust Declaration over Trust Assets for the benefit of the sukuk-holders who are participating in the business venture. The subscription of the mudharabah sukuk represents the investors’ undivided beneficial interest in the Trust Assets pursuant to their participation in the relevant venture.

The Issuer will also grant a purchase undertaking to the Trustee whereby the Issuer will acquire the sukuk upon maturity or dissolution event.

Income from the mudharabah venture will be distributed periodically as agreed. The types of mudharabah sukuk issued in the markets include short-term instrument @ commercial papers (ICP) – 1-12 months(Malaysia), medium-term instrument @ medium term notes (IMTN) – 1-5 years(Malaysia); and long-term instrument @ bond – more than 5 years.

- Musharakah transactions

- Musyarakah One is a special purpose vehicle incorporated in Malaysia under the Companies Act 1965, for the purpose of acquiring receivables from TIME Systems Integrators Sdn. Bhd. (TSI) on behalf of Musyarakah investors. Musyarakah One will issue Sukuk Musyarakah for the purpose of the said acquisition. Receivables comprise rights in, title to, interests and benefit in the payment obligations of the Government of Malaysia (GOM) to TSI pursuant to the contract to supply teaching equipment and provision of services to various schools and certain government areas, from time to time.

- Under the transaction, Musyarakah One acts as the wakeel to acquire the receivables from TSI, the purchase of which represents the sukuk holders’ undivided proportionate beneficial ownership in the payments from the GOM. The Musyarakah venture is between the sukuk holders with sharing of profit and losses based on the sukuk holders’capital contribution. The rating assigned is based upon the credit strength of the obligor, the GOM and the elimination of performance risk as receivables are securitized only upon completion of contractual obligation i.e. upon successful delivery, installation,testing and commissioning of teaching equipment.

d. Agency Based

- Sukuk wakalah transactions

- Issuer SPV issues the sukuk, which represent an undivided ownership interest in, inter alia, the wakala assets. They also represent a right of the investors against the Issuer SPV to payments of the Periodic Distribution Amounts and Dissolution Amounts.

- The Investors subscribe for the sukuk in return for a fixed principal amount (the sukuk proceeds) payable to the Issuer SPV.

- The Issuer SPV, in its capacity as principal, enters into a wakala agreement with the wakeel pursuant to which the wakeel agrees to invest the sukuk proceeds, on behalf of the Issuer SPV, in a pool or portfolio of investments (the wakala assets), selected by the wakeel, in accordance with specified criteria.

- The sukuk proceeds will be used by the wakeel to purchase the selected wakala assets from one or more sellers.

- The wakala assets will be held and managed by the wakeel, on behalf of the Issuer SPV, for the duration of the sukuk in order to generate an expected profit to be agreed upon by the principal. The wakala assets will constitute part of the trust assets held by the Issuer SPV (in its capacity as trustee) on behalf of the investors.

- The wakala assets will generate a profit return, which will be held by the wakeel on behalf of the Issuer SPV.

- The profit return will be used to fund the Periodic Distribution Amounts payable by the Issuer SPV to the Investors. Any profit in excess of the Periodic Distribution Amounts will be paid to the wakeel as an incentive fee. It is possible that the wakala assets may generate a return that is less than the Periodic Distribution Amounts. One possible mechanism used in the past, to ensure that there are sufficient funds to make up any shortfall between the income generated by the wakala assets and the Periodic Distribution Amounts due to Investors, is for the Obligor to agree (under the purchase undertaking) to purchase a certain portion of the wakala assets at regular intervals for an Exercise Price equal to the Periodic Distribution Amounts. However, following the AAOIFI Statement, the general view amongst Shari’a scholars is that it is not permissible for an Obligor to agree to purchase wakala assets for fixed or variable amounts (calculated by reference to a formula), as this would be akin to a guarantee of profit. This mechanism would only be acceptable under AAOIFI standards if the Seller and the Obligor were different entities (see “Key Features of the Underlying Structure” below).

- The Periodic Distribution Amounts will be paid to the investors on the relevant periodic distribution dates. The Periodic Distribution Amounts will either be a fixed or variable amount calculated in accordance with a fixed formula (e.g., based upon LIBOR).

- Upon

- the maturity date or upon the occurrence of an event of default, the Issuer SPV, in its capacity as trustee will exercise its option under the Purchase Undertaking to require the Obligor to purchase the wakala assets at an Exercise Price that is equal to the Dissolution Amount payable to investors together with any accrued but unpaid Periodic Distribution Amounts.

- the exercise of an optional call (if applicable) or the occurrence of a tax event, the Obligor will exercise its option under the Sale Undertaking to buy the wakala assets from the Issuer SPV, in its capacity as Trustee, at an Exercise Price that is equal to the Dissolution Amount payable to investors together with any accrued but unpaid Periodic Distribution Amounts.

- Upon the occurrence of one of the events described in (9) above, the Issuer SPV, in its capacity as Trustee, will pay the Dissolution Amount to investors using the Exercise Price received from investors and redeem the sukuk, upon which the trust will be dissolved.

2. Islamic money markets

- An Islamic money market also serves as an avenue for secondary trading of money market instruments. Depending on the objectives, risk and return preferences of money market participants, they will either buy or sell money market instruments in anticipant of obtaining investment returns. This instruments available in the money market provide investors with different levels of risk, returns and maturity.

- Instruments:-

- Al-mudharabah interbank investment.

- Islamic interbank cheque clearing system.

- Government investment certificate.

- Cagamas mudharabah bonds.

- Islamic accepted bills.

- Islamic private debt securities.

- Ar-rahnu agreement.

- Wadiah acceptance

3. Islamic forex market

- Foreign exchange (FX) is an important activity in modern economy. A foreign exchange transaction is essentially an agreement to exchange one currency for another at an agreed exchange rate on an agreed date, it provides protection against unfavorable currency exchange rates and helps businesses associated with activities in a foreign currency to set a form of currency risk exposure. And when using techniques such as foreign exchange hedging capabilities, businesses can protect against adverse currency movements at a future date. FX transactions cover foreign currency payment transactions and fund transfers involving different currencies and countries and transactions such as travelers’ cheques, foreign currency cash, foreign currency drafts, foreign currency fund transfers/remittances, investments and trade services.

- In Islamic finance, there is a general consensus among Islamic scholars on the view that currencies of different countries can be exchanged on a spot basis at a rate different from unity, since currencies of different countries are distinct entities with different values or intrinsic worth, and purchasing power. However, there were diametrically opposite views, in the past, on the permissibility of currency exchange on a forward basis, that is, when the rights and obligations of both parties relate to a future date. The divergence of views on the permissibility of currencies exchange contracts can be traced primarily to the issue of existence of the following elements; Riba (usury); Gharar (excessive uncertainty); and Qimar (speculation/gambling).

Types forex transactions:-

- A forward contract involving currencies allows one currency to be sold against another, for settlement on the day the contract expires; it eliminates the risk of fluctuating exchange rates by fixing a rate on the date of the contract for a transaction that will take place in the future.

- A futures contract involving currencies is an agreement to buy or sell a particular currency for delivery at an agreed-upon place and time in the future; however, these contracts very rarely lead to the delivery of a currency, because positions are closed out before the delivery date.

- A foreign currency option is a hedging tool, similar to an insurance policy that allows one currency to be exchanged for another on a given date, at a prearranged exchange rate, without any obligation to do so; foreign currency options eliminate the spot market risk for future transactions.

- A swap contract involving currencies is an agreement to exchange one currency for another and reverse the exchange at a later date; it is based on a notional principal amount, or an equivalent amount of principal, that sets the value of the swap at maturity but is never exchanged; Currency swaps are used to gain liquidity.

4. Islamic derivative market

- In conventional finance, hedging involves taking an offsetting position in a derivative in order to balance any gains and losses to the underlying asset. Hedging attempts to eliminate the volatility associated with the price of an asset by taking offsetting positions contrary to what customer currently has. A derivative is a financial instrument whose value depends on the value of other, more basic, variables such as grains, crude oil, palm oil, currencies, or indexes. There are four basic derivative instruments in conventional finance:

- Forward

- Future

- Option

- Swap

Instrument

- Bursa Rasmi BMBD.

d) Other financial intermediaries

- Other non-bank financial institutions accounted for the remaining 6.9% of the financial system’s total assets. They include unit trusts run by Amanah Saham Nasional Berhad (ASNB) and Amanah Saham Mara Berhad, cooperative societies,leasing and factoring companies, and housing credit institutions (comprising Cagamas Berhad, Borneo Housing Mortgage Finance Berhad and Malaysia Building SocietyBerhad).

CHAPTER 4:LEGISLATION OF ISLAMIC BANKS

BANKING AND FINANCIAL INSTITUITION ACT (BAFIA)

•Repealed and replaced the finance companies act 1969 and the banking act 1973

•Force on 1st october, 1989

•Objective - to provide new laws for the licensing and regulation of the institutions carrying on banking, finance company, merchant banking, discount house and money-broking business

•Divided into 16 part, 131 section

•Govern - Commercial banks, Finance companies, Merchant banks, Discount houses ex: Maybank, Public Merchant, HSBC

Example

•Section 124 of BAFIA, banks and Financial Institutions are allowed to operate Islamic banking or Islamic financial business and is not affected by provisions IBA.

•“Islamic financial business” means any financial business the aims and operations of which do not involve any element which is not approved by the Religion of Islam”

•Required to establish Shariah Advisory Council

•Islamic windows – section 32

Development Financial Institutions Act (DFIA)

•force on 15 February 2002

•Objective - focuses on promoting the development of effective and efficient development financial institutions (DFIs)

- to ensure that the roles, objectives and activities of the DFIs are consistent with the Government policies

•Divided into 9 part, 130 section

•Govern - Bank Pembangunan, SME Bank, Bank Rakyat, BSN

Example

•Section 129 of DFIA, prescribed institutions are allowed to operate Islamic banking or Islamic financial business and is not affected by provisions in IBA.

•“Islamic financial business” means any financial business the aims and operations of which do not involve any element which is not approved by the Religion of Islam”

•Required to establish Shariah Advisory Council

Islamic Banking Act IBA

•Objective - to provide for the licensing and regulation of Islamic banking business in Malaysia

•enables the Central Bank to supervise and regulate Islamic banks in the same way BAFIA enables it to regulate other licensed financial institutions

•Divided into 8 part, 60 section

Example

•Section 2 - “Islamic bank” means any company which carries on Islamic banking business and holds a valid license; and all the offices and branches of such a bank shall be deemed to be a bank”

•“Islamic banking business” means banking business who aims and operations do not involve any element which is not allowed by the Religion of Islam”

•Required to establish Shariah Advisory Body

Central Banking Act 2009

•Force on 23 October 1958

•Repealed Central Bank of Malaysia Act 1958

•Divided into 15 part, 100 section

•Objective - to provide for the continued existence of the Central Bank of Malaysia and for the administration, objects, functions and powers of the Bank, for consequential or incidental matters.

•- promote monetary stability and financial stability conducive to the sustainable growth of the Malaysian economy.

Example –

•Section 51

•“The Bank may establish a Shariah Advisory Council on Islamic Finance which shall be the authority for the ascertainment of Islamic law for the purposes of Islamic financial business”

Government Investment Act 1983

•Force on 11 march 1983

•Divided into 18 section

•Objective - to provide for the raising of funds by the Government of Malaysia in accordance with the Syariah principles

•- To enable the Government to receive moneys from Islamic banks for a fixed period of time. (Issue GII)

Example

•Section 2A

•“Any instruments issued under this Act shall be in accordance with the Syariah principles as approved by the Syariah Advisory Council”

REGULATION AND SUPERVISION BODY OF ISLAMIC BANKS

Syariah Supervisory Board (SSB)

- independent body of specialized jurists in fiqh al-muamalat include a member who expert in the field of Islamic financial institutions

- Objective - to ensure that Islamic Banking operation are in compliance with Islamic Shariah rules and principles

- - serves to advise the Board and management in ensuring that the Bank’s operations are in line with Shariah requirements

Role and Responsibility

- To advise the Board on Shariah matters in its business operation

- To endorse Shariah Compliance Manuals

- To endorse and validate relevant documentations

- To assist related parties on Shariah matters for advice upon request

- To advise on matters to be referred to the SAC

- To provide written Shariah opinion

- To assist the SAC on reference for advice

Malaysia Islamic Financial Center

•Launched on August 2006 as a secretariat of Bank Negara Malaysia and Securities Commission Malaysia

•Objective - to promote Malaysia as a major hub for international Islamic finance

•Focus on –

•* Sukuk origination

•* Islamic Fund and Wealth Management

•* International Islamic Bank

•* International Takaful

•* Human Capital Development (INCIEF & ISRA)

Establishment of new entities in the MIFC to conduct Islamic financial business in international currencies

•International Islamic Bank (IIB);

•International Takaful Operator (ITO)

•International Currency Business Unit (ICBU).

Islamic Financial Services Board ( IFSB)

- Started operations - 10th March 2003

- Objective –

- To promote the development of a prudent Islamic financial services industry

- To provide guidance on the effective supervision and regulation of institutions offering Islamic financial products

- To facilitate training and personnel development in skills of the Islamic financial services industry

- To establish a database of Islamic banks, financial institutions and industry experts

International Islamic Financial Markets

- the global standardization body for the Islamic Capital & Money Market segment of the IFSI.

- Objective - to encourage self-regulation for the development and promotion of the Islamic Capital and Money Market segment

- founded with the collective efforts of the

- Central Bank of Bahrain,

- Bank Indonesia,

- Central Bank of Sudan,

- Labuan Financial Services Authority (Malaysia),

- Ministry of Finance (Brunei Darussalam)

- and the Islamic Development Bank (a multilateral institution based in Saudi Arabia).

CHAPTER 5 : TECHNOLOGY, METHODOLOGY AND TOOLS ADVANCEMENT IN ISLAMIC BANKING AND FINANCE

Technology advancement in Islamic banking

- Information technology has become one of the most crucial competitive differentiators in the banking industry of the twenty-first century.

- Today’s banking business cannot exist without IT.

- Islamic banking is young in comparison to conventional banking

Evolution of technology in Islamic banking

- In the early days of Islamic banking, most of the Islamic financial institutions relied on manual processes for a small range of products and services.

- However, the need for automation comes with the increase in sophistication, data volume, complexity and cost benefits in the range of products and services.

- Internet banking

- Account information

- Funds transfer

- Bill payment

- Branch Teller System

- Transaction processing

- Cash management

- ATM

- Management information systems

- Daily/monthly report

- Managerial/operational report

- Mobile banking

- Phone banking; BIMB i-tap

- Card management

- Debit card

- Credit card

TOOLS ADVANCEMENT

Islamic Index

- An index fund is a fund, which tracks and replicates the movement of a specific financial market such as the Dow Jones. A Shariah-board choses from a specific market appropriate companies, which conform with Shariah-law.

Islamic Rating

- Rating is the evaluation or assessment of something in term of quality, quantity, or both.

- Rating agencies provide independent opinions on the credit risks and potential default risk of specific issuers. To promote transparency in the bond market, information on ratings is widely disseminated to all existing and potential private debt securities investors on a timely manner.

Islamic rating agency:

- Islamic International Rating agency http://www.iirating.com/about_profile.asp

- Rating Agency Malaysia (RAM) http://www.ram.com.my/

Chapter 6: The impact of globalization to Islamic Banking

Globalization

- Phenomenon that makes the world seem smaller in terms of human relationships due to increased development of information technology.

Globalization of Islamic Banking

- Preparation in islamic banks experiencing rapid growth in the future.

- Islamic banks should be prepared to compete with other banks in the future.

- Investment opportunities and new products should be restructured and revised to be consistent in the study of sharia board.

Positive impact

- Greater opportunities to introduce about Islamic banking.

- When there is the process of globalization of the Islamic banking sector more opportunities to introduce and give an insight into the community of the situation or the true concept of Islamic banking.

- Society will be more open to know about the Islamic banking.

- Many ways to be upgraded or enhanced to provide an opportunity for people to recognize Islamic banking.

- Greater opportunities to introduce Islamic banking product.

- Getting people to know the real Islamic banking more likely to highlight the Islamic banking sector and introduce their products.

- This opportunity should be used where possible to show that the Islamic banking products have variations from normal banks. In this way, to demonstrate the advantages of using Islamic banking products.

- Chance to enhance the using of Islamic Banking than Conventional Banking

- Introduction to Islamic banking and products used will show that there is a clear difference of Islamic banks and conventional banks.

- Differences will highlight the advantages found in Islamic bank.

Negative impact

- Become a larger of useless information

- Globalization has a lot of information that is not useful or does not apply to Islamic banking. This case, exists when a society that is more familiar to the manipulation of information abuse.

- In the future globalized world more technology invented for convenience but if abused will bring a negative impact on the world banking system Islamic information.

- Negative impression to the Non-Muslim

- In the process of dissemination of information regarding the Islamic banking sector will undoubtedly exist misunderstanding among the community

- Misunderstanding exists mainly against non-Muslims as the least able to distinguish between Islamic and conventional banking. Moreover, if not many people are Muslims themselves who wish to help them against the advantages of Islamic banking sector.

Future of Islamic Banking through globalization

- Become a major banking in Malaysia

- Islamic banking will be key in community banking in Malaysia.

- Efforts and initiatives should be enhanced to show more prominent Islamic banking banks other.

- Islamic Banking concept will become “Trading while contributing”

- Through the concept of Islamic banking, it is not only used for business or commercial help to each other.

- The main concept of the product concerned with profit:-

- Musharakah

- Mudharabah

- Takaful

- More main institutions in Malaysia

- In the future, Islamic banking will become more important institution in Malaysia.

- When this situation occurs, the public will become Islamic banking as key institutions as reference.

- Become first choice customer or attracted non-Muslim too.

- Advantages highlighted by Islamic banking institutions will be an attraction to all segments of society, including non-Muslims. This will make the institutionalization Islamic banking as the best choice.

Future of Islamic Banking and Finance through globalization

- Likely shape of Islamic Banking and Finance in Malaysia

- Islamic Banking as pure Financial Institutions

- To the original financial institutions, banking Islamic must conduct their activities in accordance with Shariah guidelines.

- Islamic banking institutions should refrain from prohibited elements such as gharar, riba and maisir.

- Standardization of Islamic Financial Products

- In the future, the Islamic banks are going through a situation of competition for products produced

- Harmonization of the concept of the products have to be adjusted in order to avoid misunderstandings community.

- Islamic Banking as pure Financial Institutions

- Structure of Islamic Finance Industry

- Normal banking institutions.

- Development finance institutions.

- Microfinance institutions.

- Funds.

- Competition

- Islamic banks need to prepare more thoroughly not only competition in the industry, but also with banks based on interest.

- Allocation of resources for the development of adequate infrastructure.

- In the a globalized world, Islamic financial institutions are faced with new challenges that need to be addressed.

- In the future, the higher the economic status and must compete with other countries.

- Allocation of resources to standardize correctly to create proper infrastructure development.

- Readiness for globalization.

- Security measures for these institutions need to be improved to avoid misunderstandings.

- Security measures need to be strengthened as well as creating a special law for the institution.

- Accelerate Islamic banking and finance law.

- Matters pertaining to the law in Islamic banking should be accelerated.

- To be compatible with what is prescribed by the board of shariah.

- Makes it easy to get extra help from the government for approval of the relevant law.

- Ensure the development of Islamic banks to mobilize potential cash flows that do not flow to the conventional banks.

- Greater emphasis to achieve financial stability.

- Achieve financial stability, emphasis should be given to items that could pose a risk.

- This is especially important for things that affect public confidence. Overall monitoring should be made more frequently.